Key Takeaways:

- DSO calculation can be a useful tool to understand the health of your receivables

- If you own a publically traded company, DSO can have a significant impact on your stock price

- “Good” DSO depends highly on your industry and payment terms

- It’s usually best to look at DSO in conjunction with ageing

- A Consistent system and collection follow-up can have a significant impact on DSO

DSO Definition

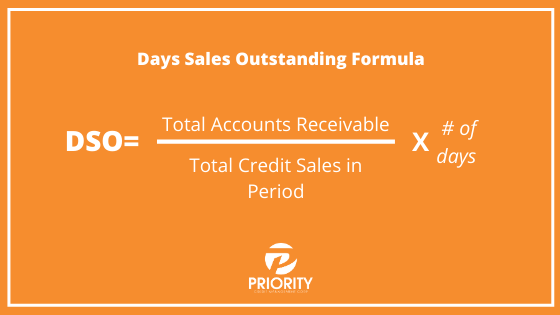

Days Sales Outstanding, or DSO calculation, is a standard key performance indicator for the number of days it takes your company to collect payment after they have made a sale. You can review your DSO on a weekly, monthly, or quarterly and depends on how important steady cash flow is to your company. Some also refer to DSO as the average collection period.

Does DSO affect your share price?

High and low DSO calculations can have a significant impact on the valuation of your business. A relatively low DSO calculation for your industry would result in premium valuations, whereas poorer DSO calculations mean you can expect a “haircut” to your valuation multiple.

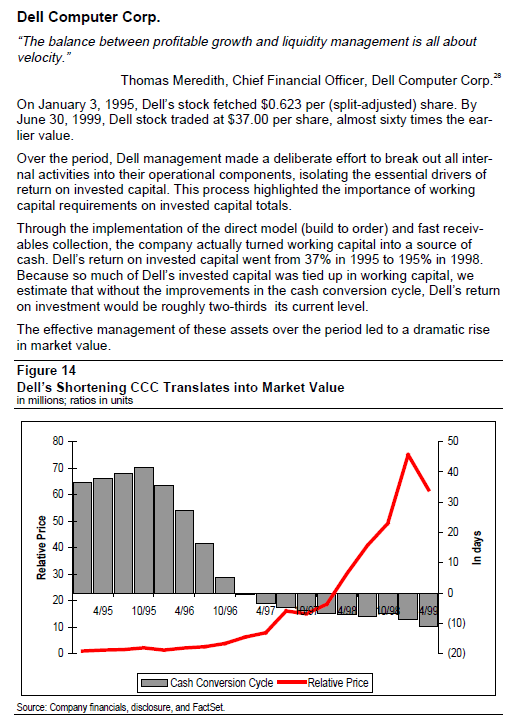

A good example of this is Dell. You can see in the chart below that by collecting quickly on their accounts receivable, they increased their cash on hand, which investors see decreases the risk of investment into the company. They have a bigger cushion and they are generating real revenues (not just booked revenues).

How to Calculate your DSO

For the average business owner and finance professional, a low DSO calculation is desirable. Here is the formula to calculate your number:

An example of DSO calculation for your business may look as follows:

ABC Corp. reports sales revenue of $3.5 million in the month of May, of which $2.5 million are credit sales, and the remaining $1 million was cash. ABC Corp.’s receivable outstanding as of the end of May was $700,000.

Given ABC Corp.’s numbers, their DSO calculation would look like this:

42= (3,500,000 / 2,500,000) x 30

In this example, ABC Corp.’s DSO calculation is 42 days. It takes, on average, 42 days for ABC Corp. to convert a credit sale into cash in the bank.

What is a “Good” DSO?

Remember that one of the biggest DSO drivers is the terms assigned. While some customers pay early - a lot will pay precisely when payment is due, and still, others pay well after that.

Say, for example, that 30-day terms are “the norm” for your industry. It is typically tricky to get a DSO that is lower than 30, and for many organizations, 30-45 days is considered a perfectly acceptable DSO. If, however, you deal with mostly 7- or 15-day terms, a 30-day DSO is well above what would be accepted by most standards.

To further clarify, DSO is best looked at in conjunction with ageing. DSO is one measure of A/R performance, as is the ageing of receivables, it helps to look at both.

If, for example, a company has a lot of 30- and 45-day accounts, they will most likely see a higher DSO calculation. That may be a bad sign. But if you see a high DSO along with a high current percentage balance (customers who pay when or before payment is due) and low amounts in past-due ageing brackets, then a high DSO makes more sense and is not necessarily cause for alarm.

Accepted DSO also depends on the size of the company. Well-capitalized companies can afford to have longer DSO, but small and medium-sized businesses can really suffer if their cash takes too long to come back. Smaller enterprises need that money to pay employees, buy raw material, and keep the lights on.

How to reduce your DSO

We prefer to use the term “control your DSO” rather than “lower your DSO.” Having full control over that number is critical. There are several things that companies can do to get high DSO numbers under control.

Examine Your Internal Processes.

A growing issue is adapting to your clients' automated payables systems. Often, you'll need internal experts who know how to manage new ways of invoicing.

If you sell to large, publicly traded companies, you will already know the challenge. Your customer will place the onus on you, the seller to correctly upload invoices, in a format acceptable to them, to their automated accounts payable system. Each customer can be using different automated payables systems, so your accounts receivable and billing staff MUST be on the ball to manage each system correctly, and edit invoices as required, to fit the unique format of each client. If the invoice is not in the correct format, it gets rejected, but no automated notification comes to you. It just sits there until one of your team logins in to check the status. If this process isn’t well documented and religiously monitored, then you can expect lengthy payment delays. If you don’t cross-train your staff on these processes, then your DSO will push higher, should a staff member leave or go on vacation. The beautiful part about these systems is, once mastered, can significantly lower your DSO, but you must be committed to learning and adapting to the new system. You can no longer mail away an invoice and hope to get paid.

Perhaps your sales team feels compelled to offer longer repayment terms to remain competitive.

Sales staff are on the front lines, and they hear customer concerns. In times of market pressures, the manipulation of credit terms is one way to make your company stand out from competitors. However, changing repayment terms may not be necessary, and your sales team is unwittingly extending your DSO by offering your customers extra time to pay. We recommend meeting with the sales team and management to come up with alternate options that don’t have you playing banker for your clients any more than necessary. If your competition is offering longer terms, and your client’s credit rating is excellent, then it is reasonable to provide the same terms. Don’t get caught in the “me too” trap. Remember, a longer DSO has many adverse effects on your cash flow. Not all customers deserve the same terms.

Your collection process is inefficient.

Sometimes a higher than average DSO is simply due to an inefficient receivable management system. All accounting systems, such as QuickBooks, Sage 50, and others, are great for accounting functions and job costing, but woefully inadequate when you must use it for staying on top of your receivables. Credit staff must be able to readily track promises, broken promises, monitor deadlines, and track other critical events like lien opportunities. Regular accounting systems do not allow for the management of the customer, so we see a significant number of companies attempting to manage their receivables using spreadsheets. Any time you begin working from records that are not part of your live data, there is room for human error. It is these errors and inefficiencies that can drive your DSO down and make the recovery of your money more cumbersome than necessary.

Push for Pre-Authorized Payments

Encourage sales to get training on Credit 101. Go through your credit application with them and explain to them how everything works.

You can train your sales team to make pre-authorizations part of their regular sales pitch. When the sales rep gets to the part about the credit application, they can say, “Here is our pre-authorized payment form. I’ll need a "void" cheque also...”

If the client balks, your sales rep can explain that they would need to bring it back to credit and that they would need to take a further dive into their credit app for special approval. Usually, that does the trick.

Include pre-authorized payments in the sales process, don’t ask for it.

A word of caution: not all customers should be put on a pre-authorized payments. It is important to remember that pre-authorized payments do not guarantee funds, so assessing creditworthiness is always important. It is also important to assign pre-authorized terms that do not create excessive risk exposure by allowing your customer too much time to rack up their balance between pre-authorized payment runs.

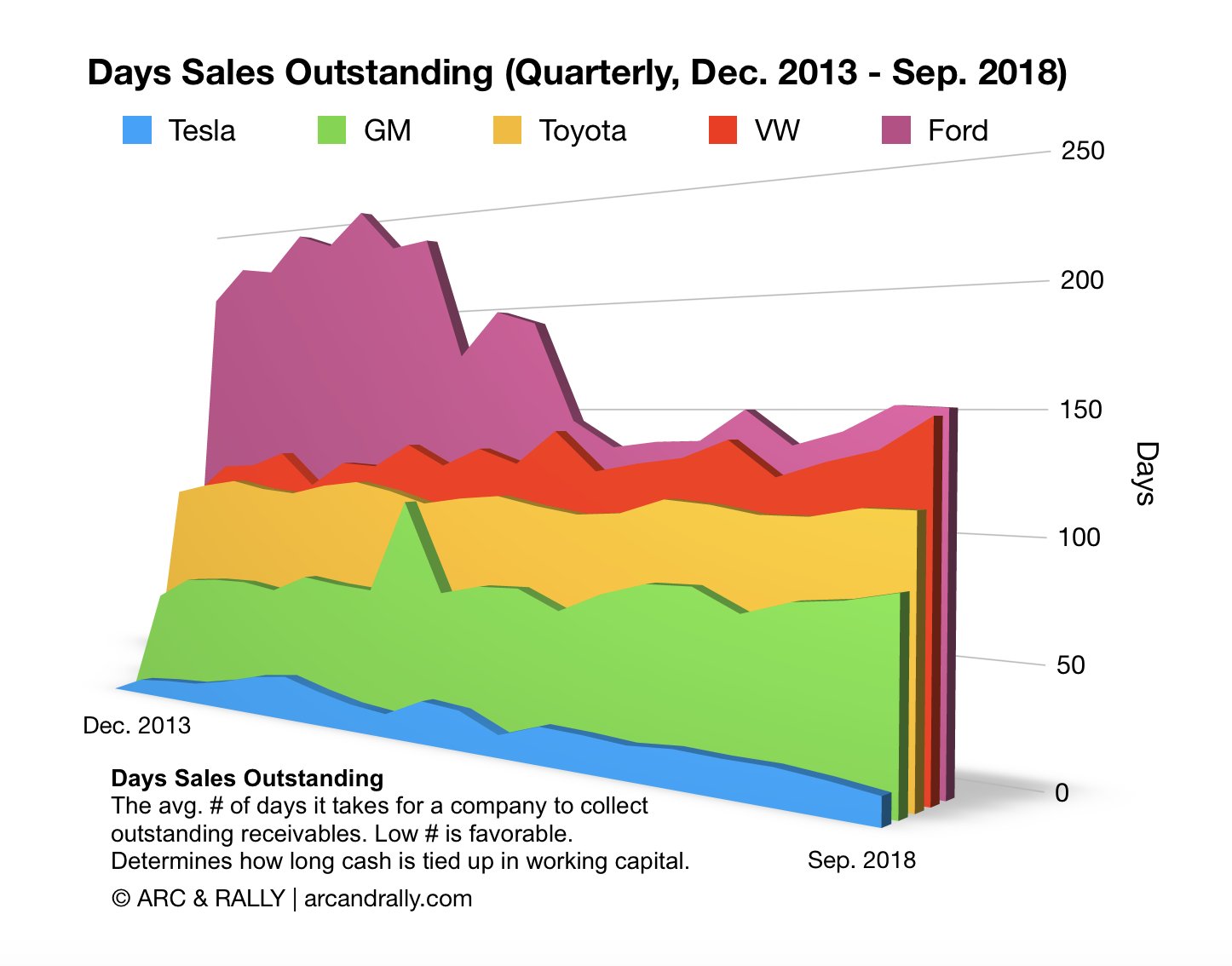

We found this graph interesting given that Tesla is such a new company that generates a fraction of revenue of the "Big Four" automakers noted here. Part of what keeps their DSO around 11 days, compared to the industry "standard" of 75-150 days, is that Tesla's customers pay BEFORE materials are ordered and the car is built. Tesla has the customer’s money before anything is done.

Get Brand New Businesses on COD.

If you’re planning on extending credit to a brand new business, typically they are not good candidates for pre-authorized payments as they seldom will have the cash upfront. Collecting on delivery is a way to ensure you build a level of trust with the new business, without expecting them to set up pre-authorized payments immediately after business start-up.

Build relationships with your competitor’s credit managers and share insights. Stay on top of industry news and trends, use credit reporting agencies, seek out industry credit groups for information. The key is to stay connected with what is happening in your business.

Make Sure Your Terms are Sensible

Pay attention to the industry you are serving. For example, if your customer is a major hotel chain, and your terms are seven days, to expect them to pay you in 7 days is not practical, as their internal processes will not allow this. Your receivables ageing may be "skewed" as a result of this, making it harder to understand DSO trends.

Consistent Collection Follow Up

Many steps will form a substantial credit and collection policy handbook, and consistent collection follow up is one of the main methods of reducing your DSO. A few things to consider as part of your collection process are:

1. Grab the Low Hanging Fruit

DSO is a weighted average of the payment patterns of both risk and non-risk customers. Non-risk customers might take advantage of early payment discounts or even pay before the due date. The influx of cash from these customers, especially those whose purchases are large, can have a significant impact on days sales outstanding. The effect can be both positive or negative. Therefore, it is essential that your credit department has the desire and ability to monitor payments from large customers and begin immediate follow up in the event of an uncharacteristic delay. Lowering or reducing DSO is contingent on your collection efforts on both risk and non-risk customers. Don’t get hung up on your chronic past-due customers only.

2. Automate Your Invoicing Process (If you haven’t already)

While billing on time doesn’t guarantee payment on time, many organizations find that utilizing a service like Intuit’s automated billing creates more consistent payments from their customers. Also, you save time on processing, putting more money back into your pocket, while serving your customers. Do not let inaccurate or untimely billing be the cause of a higher DSO.

3. Try Demand Letters

A practical method of maintaining consistent collection efforts to reduce DSO is to issue a collection or demand for payment letter on every past due invoice. The constant communication to your customer that invoices are outside your credit terms can serve to educate habitually late payers into paying on time. Many firms who do not regularly follow up immediately upon an invoice becoming past-due also inform customers that it is okay to be late with a payment. The squeaky wheel gets the grease.

4. Enlist Collections at the Right Time

And finally, a few words about the use of third parties (primarily collection agencies.) All grantors of credit must accept the fact that there will be times when the introduction of a third-party is necessary to recover funds owed. For reasons unexplained, the use of a collection agency brings about the feelings of failure for some credit professionals. As a consequence, the use of a third-party to reduce DSO is sometimes delayed far beyond the point where effective action could have produced positive results. When facing an imminent potential loss, an agency should be engaged immediately if your initial demands for payment go answered.

The Bottom Line

The bottom line that matters is your bottom line. DSO calculation is an excellent tool to help you manage the financial health of your company as well as the efficiency of your accounts receivable systems.

It is the consistent and persistent communication with your customers that will have the most positive effect of reducing your DSO. As soon as one begins to give extra time to specific customers and not the whole portfolio, your DSO can get away on you, and it’s tough to re-educate those customers to get back on side.

Efficient cash flow systems boost the profitability of your business and your company’s overall value.

Co-Author: Rola Pyper

Over the years I have accumulated management experience in Customer Service, Office Management, Accounts Payable, as well as Accounts Receivable, Credit & Collections. Through these roles, I have come to understand many aspects of different industries such as fitness, construction, food supply, property management, and camp and catering. I believe that this exposure to many different industries is very useful in my role as Production Manager, Credit Coordinators for PCM.